Truckload Freight Rates Forecast Q1 2023 Update

Arrive Insights® team generated this forecast through a combination of extensive historical research and output from the predictive models built into ARRIVEnow

High Level Q1 Recap

Overall, rate movements have aligned with the forecast we released in October 2022. Although the market experienced more volatility than expected during the 2022 holiday season and early January 2023, conditions have fallen in line with where we projected they would be late in Q1 2023. Downward pressure on rates persists as the economy and truckload demand normalize toward pre-pandemic levels. Additionally, surplus capacity accumulated over the last few years should drive a prolonged period of spot market equilibrium and deflationary contract rates as the gap between the two closes.

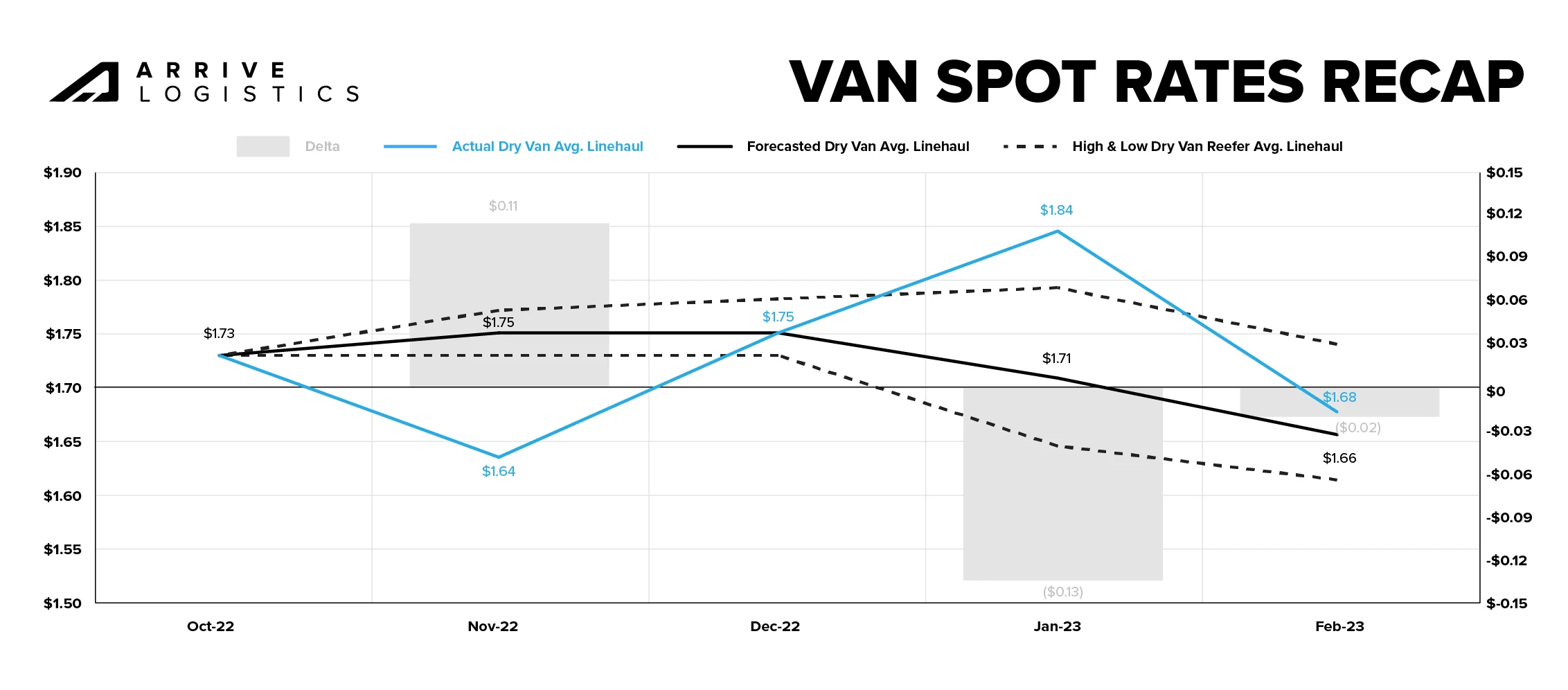

Van Spot Rates Recap

November van spot rates declined rapidly and landed short of expectations due to reduced retail demand and excess inventory buildup ahead of the holiday season. However, in December, rates rebounded as expected, thanks to a demand surge and seasonal capacity constraints caused by the holidays and winter weather disruptions.

The market disruption persisted longer than predicted, leading to a slight deviation from our forecast in January. However, rates quickly fell back in line with expectations later in January and into February, so the forecast error for February was just $0.02 off of our initial projections.

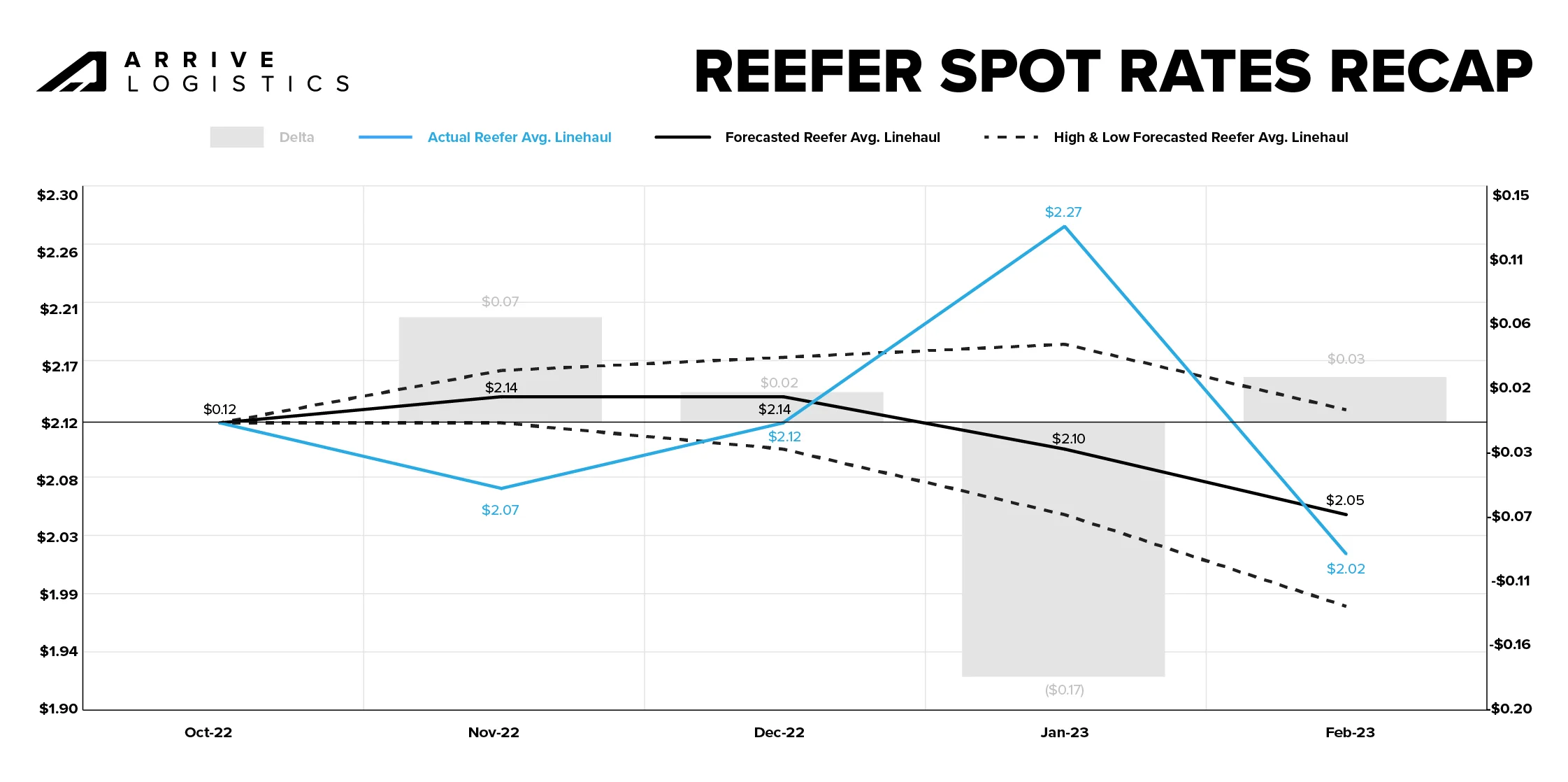

Reefer Spot Rates Recap

Reefer spot rates followed a similar trend to van spot rates for the same period. Following a slow November, December rates aligned with our forecast once extreme weather and seasonal capacity constraints set in around the holidays. The disruption persisted into January, driving a slight deviation from our forecast during that time.

The gradual rate movement we predicted for January and February happened significantly faster than anticipated, bringing rates back in line with our October 2022 projections and creating a nominal forecast error of just $0.03. Fuel also had a similar impact on reefer spot rates as van spot rates.

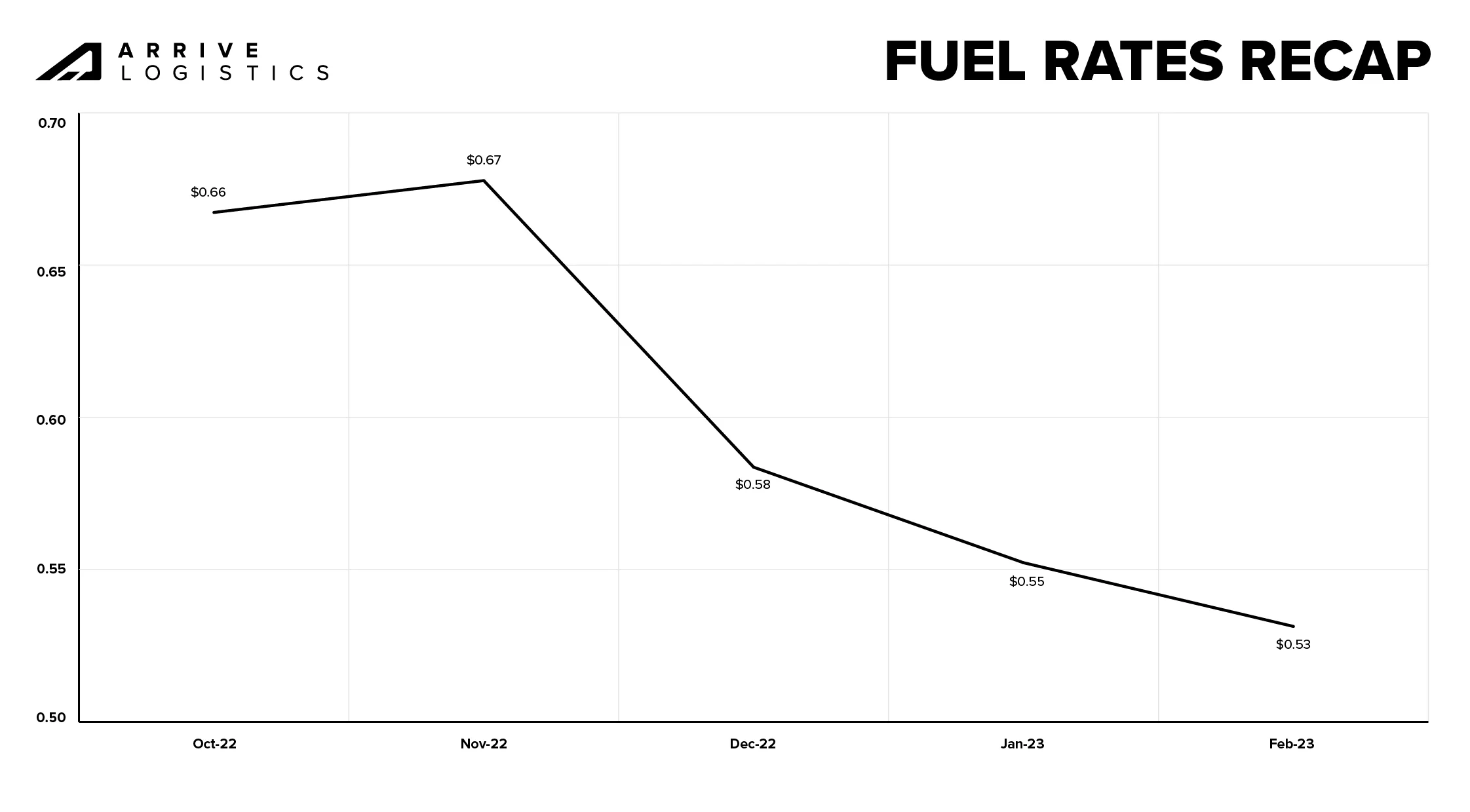

Fuel Rates Recap

Spot rates are typically negotiated as all-in rates, so rapid fuel price fluctuations can contribute to forecast errors. For example, the significant $0.14 per mile decline in the average fuel surcharge from November 2022 to February 2023 likely led to temporary volatility in our forecast. Fuel prices have since stabilized, resulting in rates that align closely with our original projections.

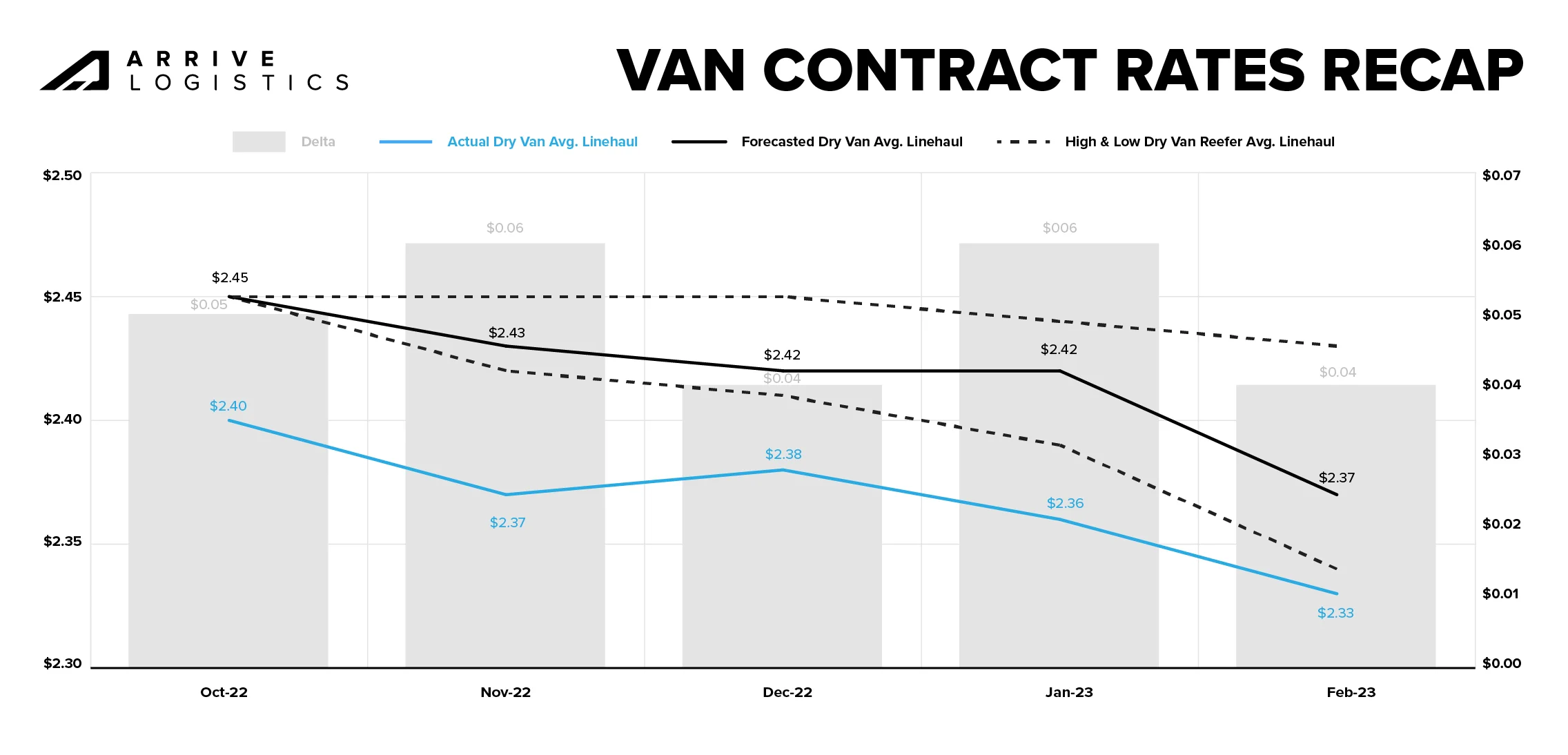

Van Contract Rates Recap

At the beginning of November 2022, DAT reported the October van contract rate to be $2.45 per mile, excluding fuel. As the month went on, that number adjusted to $2.40 per mile, excluding fuel. Though such adjustments are not uncommon in DAT data, ones of this size are, and it shifted our contract rate baseline by $0.05 before the forecast even went live.

With that in mind, we recommend reviewing the monthly predicted rate movements when using this forecast for planning purposes. For example, for October 2022 to February 2023, we forecasted contract rates, excluding fuel, to fall between $0.02 and $0.11 per mile, with a decline of $0.08 per mile being the most likely scenario. The actual rate decline was $0.07 per mile, meaning our forecast was within $0.01 per mile of actual contract rate movements.

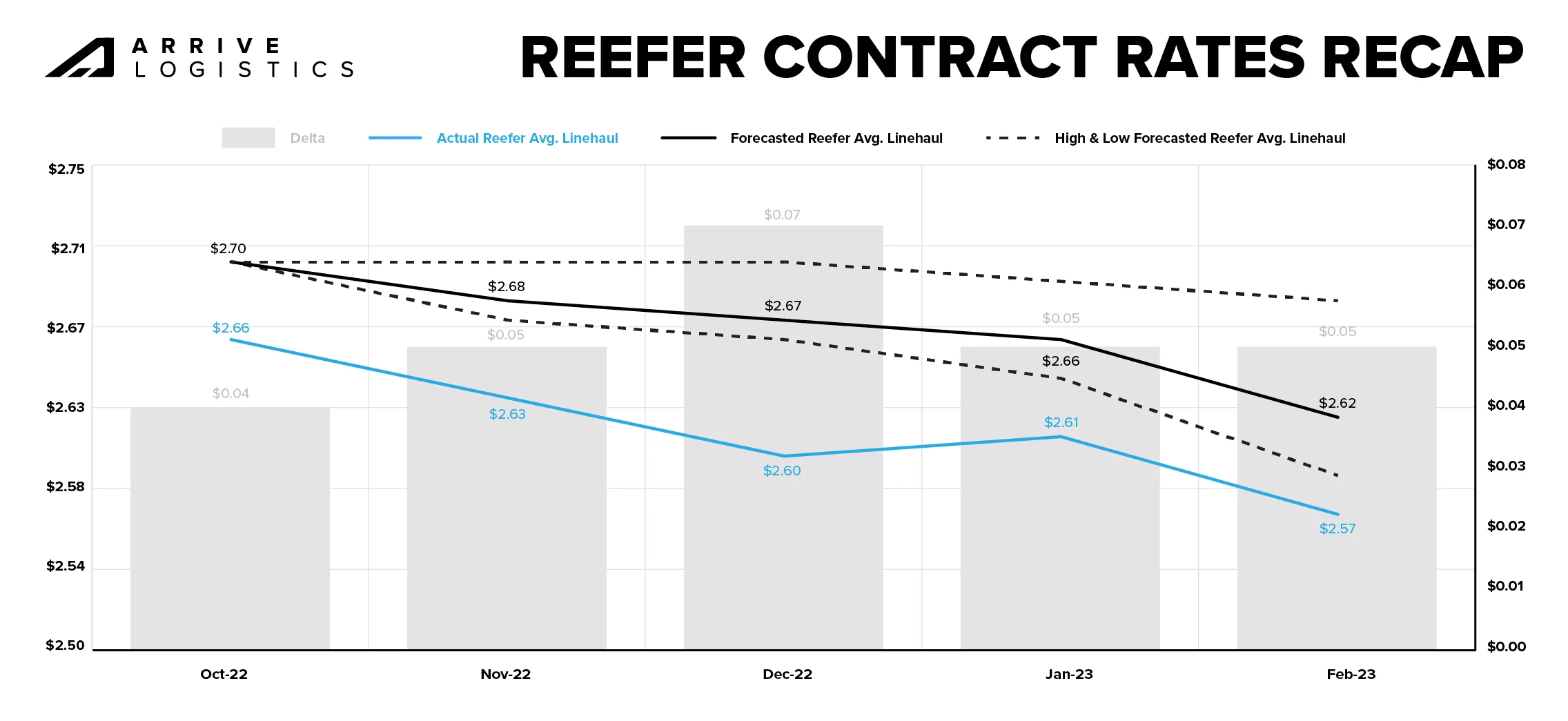

Reefer Contract Rates Recap

DAT reefer contract rate data showed a similar adjustment to van contract rates in October 2022. Thus, the same baseline adjustment rule applies here. From October to February, we forecasted contract rates, excluding fuel, to fall between $0.02 and $0.11 per mile, with a decline of $0.08 per mile being our most likely scenario. The actual rate decline was $0.09 per mile, meaning our forecasted rate movement was within $0.01 per mile of actual contract rate movements.

2023 Rate Forecast

Q1 Update

Truckload Freight Outlook

Rates

We expect spot rates to remain relatively stable as contract rates continue normalizing and the gap between the two gradually closes throughout the year. Demand will likely outpace capacity exiting the market in the short term, so strong routing guide compliance should continue. However, current conditions will lead to carriers right-sizing their fleets in response to downshifts in demand, which may drive enough capacity out of the market that it becomes vulnerable to widespread severe weather, demand surges or other disruptive events.

Supply

Capacity will continue to be established on contract freight, and shippers can expect ongoing strong routing guide performance. Significant capacity was added to the market during the last inflationary rate cycle, with total employment in long-haul trucking recently reaching an all-time high. Record numbers of owner-operators and small carriers are shutting down; however, market capacity remains ample as many take company jobs with larger assets rather than leaving the industry entirely. Strong routing guide compliance through the summer 2022 peak season and at the onset of Q4 2022 provided additional confidence that capacity is sufficient to support current demand. 2023 RFP season awards are expected to be smaller than a year ago, leaving many carriers without enough freight to support current staffing levels — this could be the first sign of declining trucking employment growth.

Demand

Overall freight tonnage will likely decline further as economic conditions normalize toward pre-pandemic levels. Current truckload demand is healthy compared to historical norms, but strong routing guide performance continues to drive significant spot market demand declines. Rising interest rates have already slowed housing markets, which, in turn, means fewer goods purchases and slowing demand. Ongoing inflation will likely continue to drive down consumer spending on goods. Declining manufacturing orders and weak retail import forecasts will increase downside risk for the demand outlook.

To see full report and learn more about Arrive visit here

Category: Featured, General Update, News

Subscribe

If you enjoyed this article, subscribe to receive more just like it.