2023-Ending Data Suggest Moderating Trailer Activity in 2024

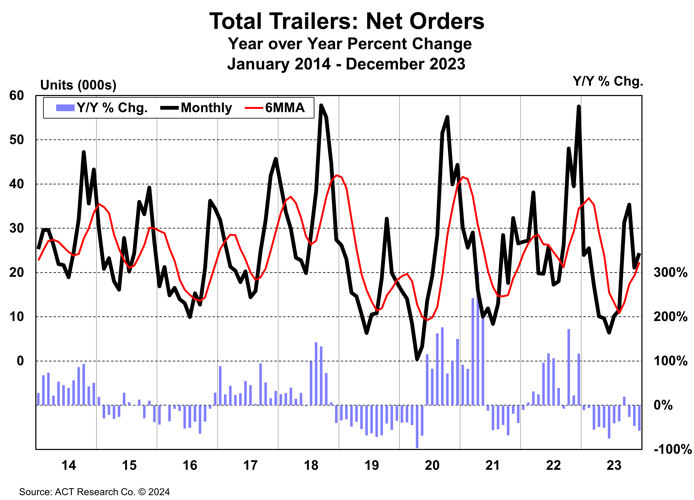

ACT Research reports December net orders, at 24,300 units, were nearly 58% lower y/y, but 3,300 units more than were booked in November

With freight markets continuing their bounce along the bottom, carrier profits at a low ebb, and pent-up demand exhausted, the 2024 game plan is more about hoping and coping than full steam ahead for the trailer market, according to this month’s issue of ACT Research’s State of the Industry: U.S. Trailers report.

December net orders, at 24,300 units, were nearly 58% lower y/y, but 3,300 units more than were booked in November.

“With 35% of the year’s orders historically booked in Q4, the quarter’s seasonal factors run roughshod on the nominal data. Seasonally adjusted, December’s orders fall to 17,200 units, a 206k SAAR” said Jennifer McNealy, Director–CV Market Research & Publications at ACT Research. “Dry van orders contracted 87% y/y, with reefers down 56%, and flats 75% lower compared to December 2022.”

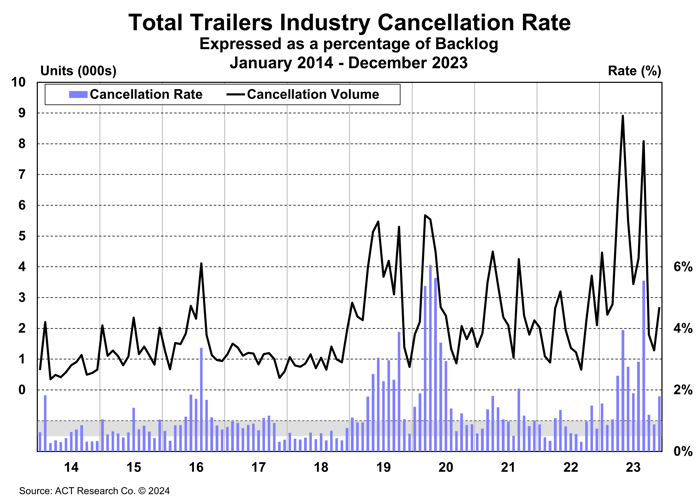

She added, “Total cancellations increased to 1.7% of the backlog

from November’s 0.9%, elevated for most segments and much higher for some. Digging down, several markets were again above 1.0%, including dry vans at 1.3%, flats at 3.5%, medium lowbeds at 1.5%, and dumps at 1.3%. Both tank categories reported a spike in cancellations, both around 7% of the backlog. Recent oil price weakness may bear some culpability.”

McNealy concluded, “December’s backlog-to-build ratio was squeezed by a stronger build rate offset by only a slight uptick in backlog. This combination of events resulted in a lower 2023-ending backlog-to-build ratio, at 5.3 months now versus the 5.8 months in November.”

Category: Cab, Trailer & Body, Cab, Trailer & Body New, Equipment, Featured, General Update, News, Products, Vehicles

Subscribe

If you enjoyed this article, subscribe to receive more just like it.